Status, Drivers & Barriers

Green hydrogen is an energy carrier that can be used in many different applications. However, its actual use is still very limited. Each year around 120 million tonnes of hydrogen are produced globally, of which two-thirds are pure hydrogen and one-third is in a mixture with other gases (IRENA, 2019a). Hydrogen output is mostly used for crude oil refining and for ammonia and methanol synthesis, which together represent almost 75% of the combined pure and mixed hydrogen demand.

Today’s hydrogen production is mostly based on natural gas and coal, which together account for 95% of production. Electrolysis produces around 5% of global hydrogen, as a by-product from chlorine production.

Currently, there is no significant hydrogen production from renewable sources: green hydrogen has been limited to demonstration projects (IRENA, 2019a).

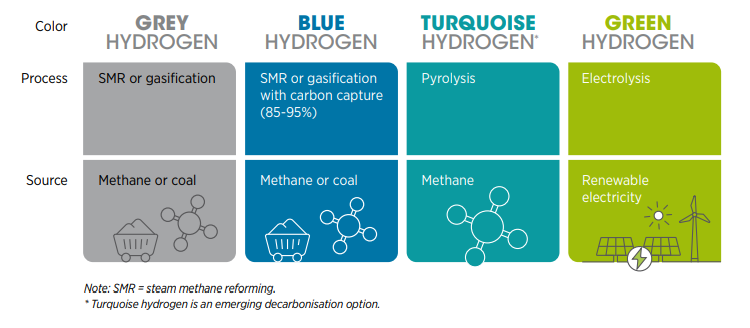

DIFFERENT SHADES OF HYDROGEN

Hydrogen can be produced with multiple processes and energy sources; a colour code nomenclature is becoming commonly used to facilitate discussion.

But policy makers should design policy using an objective measure of impact based on life-cycle greenhouse gas (GHG) emissions, especially since there might be cases that do not fully fall under one colour (e.g. mixed hydrogen sources, electrolysis with grid electricity).

DRIVERS OF THE NEW WAVE OF GREEN HYDROGEN

There have been several waves of interest in hydrogen in the past. These were mostly driven by oil price shocks, concerns about peak oil demand or air pollution, and research on alternative fuels. Hydrogen can contribute to energy security by providing another energy carrier with different supply chains, producers and markets; this can diversify the energy mix and improve the resilience of the system. Hydrogen can also reduce air pollution when used in fuel cells, with no emissions other than water. It can promote economic growth and job creation given the large investment needed to develop it as an energy carrier from an industrial feedstock.

As a result, more and more energy scenarios are giving green hydrogen a prominent role, albeit with significantly different volumes of penetration. The new wave of interest is focused on delivering low-carbon solutions and additional benefits that only green hydrogen can provide.

The drivers for green hydrogen include:

Low variable renewable energy (VRE) electricity costs

The major cost driver for green hydrogen is the cost of electricity. The price of electricity procured from solar PV and onshore wind plants has decreased substantially in the last decade. In 2018, solar energy was contracted at a global average price of 56 USD/MWh, compared with 250 in 2018. Onshore wind prices also fell during that period, from 75 USD/MWh in 2010 to 48 in 2018 (IRENA, 2019b). New record-low prices were marked in 2019 and 2020 around the world: solar PV was contracted at USD 13.12/MWh in Portugal (Morais, 2020) and USD 13.5/MWh in the United Arab Emirates (Abu Dhabi) (Shumkov, 2020); onshore wind was contracted at USD 21.3/MWh in Saudi Arabia (Masdar, 2019) while in Brazil, prices ranged between USD 20.5 and 21.5/MWh (BNEF, 2019). With the continuously decreasing costs of solar photovoltaic and wind electricity, the production of green hydrogen is increasingly economically attractive. (Box : challenges for green Hydrogen)

Challenges for Green Hydrogen

Despite the Green H2 potential to replace non-renewable energy sources in short, medium and long terms, there are issues that still need to be overcome for the application of the Green H2 technology:

The cheaper the energy utilized to generate green hydrogen, the most viable it will be to expand the production chain. Investments in increase of scale and efficiency in the production of wind and solar energy are being directed towards the regions with the most potential in the planet.

In this context, China, Mongolia, Australia, Morocco and Chile stand out.

An integrated commercial plant will be built in the latter for industrial-scale production of climate-neutral fuel (e-fuel), from the combination of hydrogen produced from wind power and CO2 captured from the air. Named “Haru Oni”, the project will have investments from the German federal government in the order of € 8.23 million and it counts on several international partners.

Nowadays, green hydrogen is two to three times more expensive than blue hydrogen. It is estimated that the production costs for green hydrogen could fall by up to 62% until 2030, to something close to a level from US$ 1.4 to US$ 2.3 per kg. If this occurs, the parity between the cost of green hydrogen and the one of gray hydrogen can happen somewhere between 2028 and 2034 – with projections below US$ 1 per kg in 2040.

Technologies ready to scale up

Many of the components in the hydrogen value chain have already been deployed on a small scale and are ready for commercialisation, now requiring investment to scale up. The capital cost of electrolysis has fallen by 60% since 2010 (Hydrogen Council, 2020), resulting in a decrease of hydrogen cost from a range of USD 10-15/kg to as low as USD 4-6/kg in that period.

Many strategies exist to bring down costs further and support a wider adoption of hydrogen (IRENA, forthcoming).

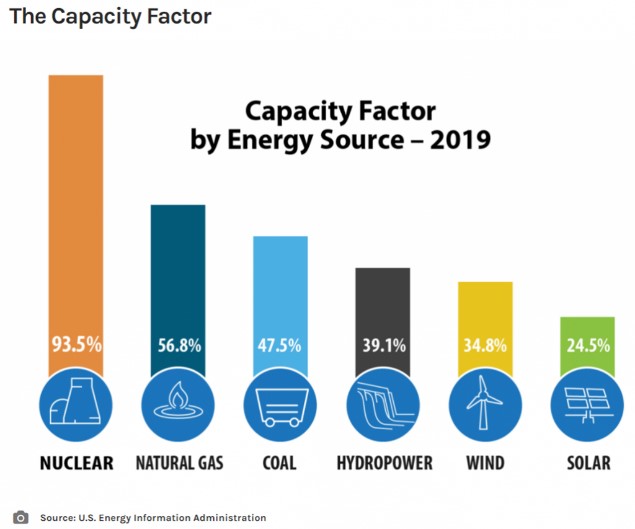

The cost of fuel cells for vehicles* has decreased by at least 70% since 2006 (US DOE, 2017). While some technologies have not been demonstrated at scale yet (such as ammonia-fuelled ships) (IRENA, 2020b), scaling up green hydrogen could make those pathways more attractive as production costs decrease. (Box: Variability and intermittence of wind and photovoltaic and Box: capacity factor)

The capacity factor varies widely from energy source and technology. In the case of renewables such as wind and photovoltaics, it is also necessary to consider that the capacity factor depends from place to place based on variables such as windiness, irradiation and hours of light.

*Fuel cells use the same principles as an electrolyser, but in the opposite direction, for converting hydrogen and oxygen into water in a process that produces electricity. Fuel cells can be used for stationary applications (e.g. centralised power generation) or distributed applications (e.g. fuel cell electric vehicles). Fuel cells can also convert other reactants, such as hydrocarbons, ethers or alcohols

Variability and intermittence of wind and photovoltaic

Wind and photovoltaic are the technologies on which the greatest expectations of an energy transition towards the so-called after-fossil are commonly placed. Variability and intermittence are a major limitation, as well as a cause of greater complexity of the electrical systems and consequent need for adaptation. To better understand what we are talking about when we talk about a strongly intermittent and variable electricity supply, the box presents the recordings of the power produced by wind and photovoltaic plants in Relationship with geographic and climatic situations (See box Capacity Factor).

Capacity factor

Electricity production from wind and photovoltaics shows strong variations over the course of the year, month, day and even in a single hour A fundamental measure to understand intermittent renewables such as photovoltaic and wind is the capacity factor , i.e. the ratio between the electricity actually produced in a given period of time and the nominal generation power of the plant. The capacity factor can be expressed in hours or as a percentage of the time of the specific period considered necessary for the nominal power of the plant to supply the total energy actually produced. A plant with a capacity factor of 100% means that it produces energy at all times. There is also talk of equivalent hours (generally one year) to produce the total energy actually produced with the nominal power.

The capacity factor varies widely from energy source and technology. In the case of renewables such as wind and photovoltaics, it is also necessary to consider that the capacity factor depends from place to place based on variables such as windiness, irradiation and hours of light.

Benefits for the power system

As the share of VRE rapidly increases in various markets around the world, the power system will need more flexibility*.

The electrolysers used to produce green hydrogen can be designed as flexible resources that can quickly ramp up or down to compensate for fluctuations in VRE production, by reacting to electricity prices (Eichman, Harrison and Peters, 2014). Green hydrogen can be stored for long periods, and can be used in periods when VRE is not available for power generation with stationary fuel cells or hydrogen-ready gas turbines. Flexible resources can reduce VRE curtailment, stabilise wholesale market prices and reduce the hours with zero or below zero electricity prices (or negative price), which increases the investment recovery for renewable generators and facilitates their expansion. Finally, hydrogen is suitable for long-term, seasonal energy storage, complementing pumped-storage hydropower plants. Green hydrogen thus supports the integration of higher shares of VRE into the grid, increasing system efficiency and cost effectiveness.

*System flexibility is here defined as the ability of the power system to match generation and demand at any timescale

Government objectives for net-zero energy systems.

By mid-2020, seven countries had already adopted net-zero GHG emission targets in legislation, and 15 others had proposed similar legislation or policy documents. In total, more than 120 countries have announced net-zero emissions goals (WEF, 2020). Among them is the People’s Republic of China (hereafter “China”), the largest GHG emitter, which recently pledged to cut its net carbon emissions to zero within 40 years. While these net-zero commitments have still to be transformed into practical actions, they will require cutting emissions in the “hard-to-abate” sectors where green hydrogen can play an important role.

Broader use of hydrogen

Previous waves of interest in hydrogen were focused mainly on expanding its use in fuel cell electric vehicles (FCEVs). In contrast, the new interest covers many possible green hydrogen uses across the entire economy, including the additional conversion of hydrogen to other energy carriers and products, such as ammonia, methanol and synthetic liquids. These uses can increase the future demand for hydrogen and can take advantage of possible synergies to decrease costs in the green hydrogen value chain. Green hydrogen can, in fact, improve industrial competitiveness, not only for the countries that establish technology leadership in its deployment, but also by providing an opportunity for existing industries to have a role in a low-carbon future. Countries with large renewable resources could derive major economic benefits by becoming net exporters of green hydrogen in a global green hydrogen economy.

Interest of multiple stakeholders

As a result of all the above points, interest in hydrogen is now widespread in both public and private institutions. These include energy utilities, steel makers, chemical companies, port authorities, car and aircraft manufacturers, shipowners and airlines, multiple jurisdictions and countries aiming to use their renewable resources for export or to use hydrogen to improve their own energy security. These many players have also created partnerships and ongoing initiatives to foster collaboration and co-ordination of efforts*.

*The Hydrogen Council is an example of a private initiative. Launched in 2017, it has 92 member companies (by October 2020). The Hydrogen Initiative under the Clean Energy Ministerial is an example of a public initiative, where nine countries and the European Union are collaborating to advance hydrogen. The Fuel Cell and Hydrogen Joint Undertaking is an example of private-public partnership in the European Union.

However, green hydrogen still faces barriers.

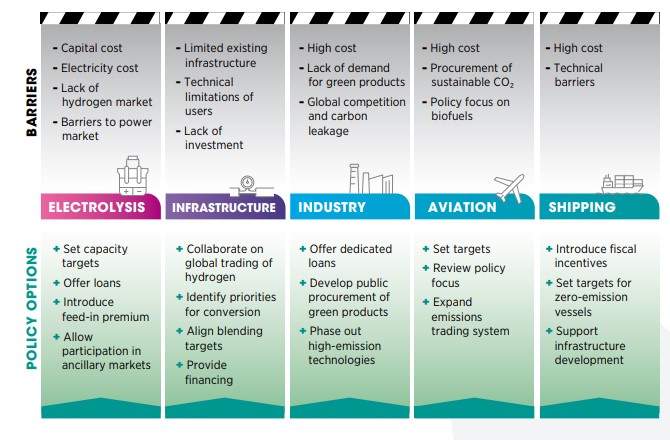

BARRIERS TO THE UPTAKE OF GREEN HYDROGEN

There have been several waves of interest in hydrogen in the past. These were mostly driven by oil price shocks, concerns about peak oil demand or air pollution, and research on alternative fuels. Hydrogen can contribute to energy security by providing another energy carrier with different supply chains, producers and markets; this can diversify the energy mix and improve the resilience of the system. Hydrogen can also reduce air pollution when used in fuel cells, with no emissions other than water. It can promote economic growth and job creation given the large investment needed to develop it as an energy carrier from an industrial feedstock. As a result, more and more energy scenarios are giving green hydrogen a prominent role, albeit with significantly different volumes of penetration (see Box 1.1). The new wave of interest is focused on delivering low-carbon solutions and additional benefits that only green hydrogen can provide. The drivers for green hydrogen include:

- High production costs

- Lack of dedicated infrastructure

- Energy losses

- Lack of value recognition

- Need to ensure sustainability

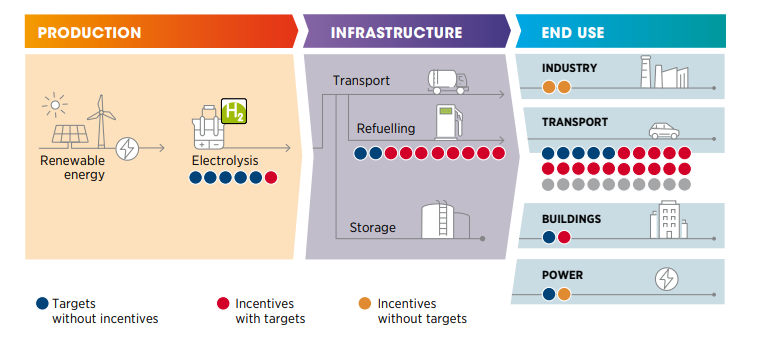

POLICIES TO SUPPORT GREEN HYDROGEN

Historically, every part of the energy system has enjoyed some form of policy support. This has been and is still true for fossil fuels (which are supported with both direct and indirect subsidies) and for renewable energy sources, across all sectors – power, heating and cooling, and transport (IRENA, IEA and REN21, 2018). The hydrogen sector has also received some attention from policy makers with dedicated policies. But more dedicated policy support is needed at each stage of technology readiness, market penetration and market growth.

Status of policy support for green hydrogen

By 2019, hydrogen was being promoted in at least 15 countries and the European Union with supporting policies (other than standardisation processes or national strategies)*.

These policies directly or indirectly promoted hydrogen use across various end uses. However, due to previous focus on land transport uses for hydrogen, about two-thirds of the policies targeted the transport sector.

Most countries include FCEVs with battery electric vehicles in their zero-emission vehicle policies. This gives FCEVs the opportunity to benefit from incentives given to zero emission vehicles in general, without the need for policies that specifically promote hydrogen use.

The past two years, however, represented a game-changing moment for green hydrogen policies, with interest rising around the world. Many countries (including Austria, Australia, Canada, Chile, France, Germany, Italy, Morocco, the Netherlands, Norway, Portugal and Spain, along with the European Union) announced, drafted or published national hydrogen strategies and post-COVID-19 recovery packages that included support measures for clean hydrogen.

*Belgium, Canada, China, France, Germany, Iceland, Italy, Japan, the Netherlands, Norway, New Zealand, Republic of Korea, Spain, United Kingdom and United States.

The stages of green hydrogen policy support

As the penetration of green hydrogen technologies increases and costs come down, policies will have to evolve accordingly. The briefs following this report use the concept of policy stages to reflect the evolution of policy needs with the increased deployment of green hydrogen. Here are the three basic stages and the overall milestones for each:

- First stage: Technology readiness

- Second stage: Market penetration

- Third stage: Market growth

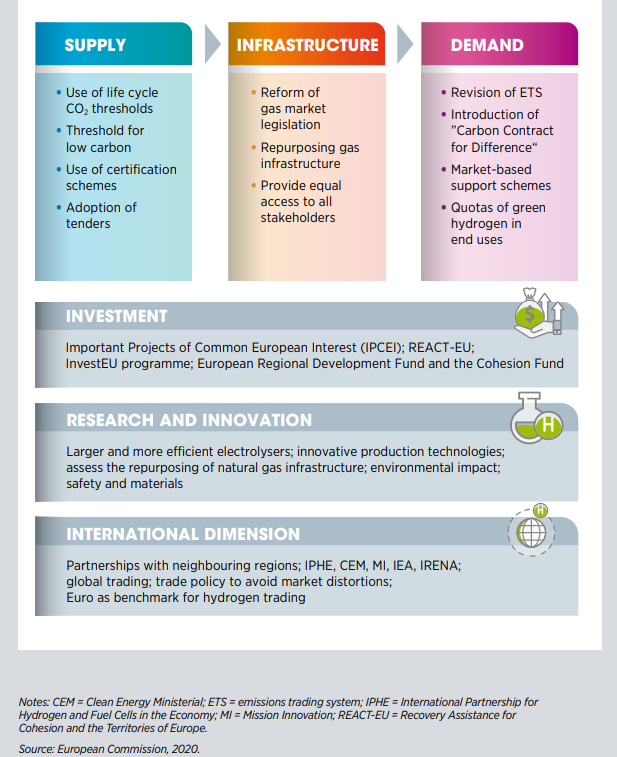

POLICY PILLAR 1: NATIONAL STRATEGIES

Recently announced hydrogen strategies result from a long process and mark the beginning of a new wave of policies. The strategy process usually starts with the establishment of R&D programmes to understand the fundamental principles of the technology, to develop the knowledge base that will inform future stages, and to explore multiple technologies and possibilities given that, at this early stage, the end applications are far from clear.

The next step is usually a vision document that clarifies the “why”: “why hydrogen”, “why this jurisdiction”, and “why now”.

The vision document represents a beacon that guides research, industry efforts and early demonstration programmes. Such vision documents are often co-created by governments and private actors attracted by the growth prospects of breakthrough applications.

Next is a roadmap that goes one step further.

It defines an integrated plan with the activities needed to better assess the potential for hydrogen. It identifies the short-term actions needed to advance deployment, and defines the research areas with the highest priority and the applications where demonstration projects are most needed.

Finally, the strategy itself defines the targets, addresses concrete policies and evaluates their coherence with existing energy policy.

The strategy covers not only specific direct policies (such as feed-in premiums for green hydrogen), but also includes integrating and enabling policies that are needed to ensure deployment across the system, such as those that support the development of a skilled workforce. The strategy is informed by extensive scenario modelling, often with input from academia and industry. It sets the level of ambition that will guide the work in subsequent stages.

Throughout the process of preparing the strategy, public-private partnerships are often formed. They serve as a platform to exchange information to advance technological progress, create consensus, align views, develop incentives and co-ordinate activities. Public-private partnerships can reduce the risks during early deployment, facilitating the transition from demonstration to commercialisation.

They allow companies to build experience while providing the benefits of first-mover advantage in case of success. The objective should be to reach a point where no further public support is needed. This model has already been successful in mobility and in the European Union (through the Fuel Cells and Hydrogen Joint Undertaking) to demonstrate hydrogen technologies for multiple pathways.

POLICY PILLAR 2: ESTABLISH POLICY PRIORITIES FOR GREEN HYDROGEN

Individual countries have specific conditions.

As a result, national green hydrogen policy makers should carefully assess, in order to set up their policy priorities, key factors for each segment of the hydrogen value chain.

These include the size of the country’s renewable resources, the maturity of its energy sector, the current level of economic competitiveness and the potential socio-economic effects.

For example, a region with good renewable energy resources could use electrolysis to make green hydrogen cost-competitive, while in other cases policy makers may identify more value in importing hydrogen instead and focusing their efforts on other technologies underpinning the energy transition.

As countries develop their net-zero emission and green hydrogen strategies, it may be useful to remember three basic concepts to set up policy priorities.

POLICY PILLAR 3: GUARANTEE OF ORIGIN SCHEME3

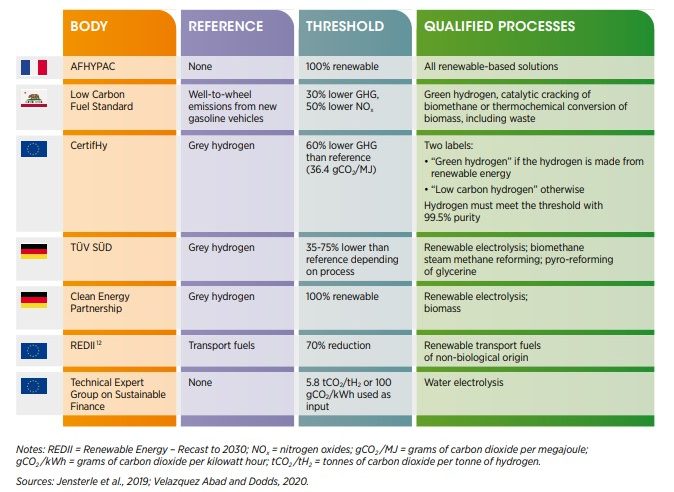

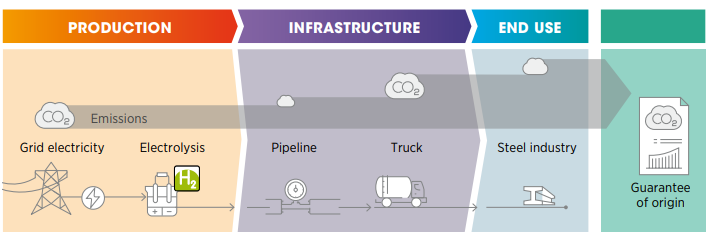

Molecules of green hydrogen are identical to those of grey hydrogen. For this reason, once hydrogen has been produced, a certification system is needed that allows end users and governments to know the origin and quality of the hydrogen.

The schemes used to track origin are usually referred to as providing a “guarantee of origin” (GO)*. One example in the case of hydrogen is the CertifHy project in the European Union. The scheme issued over 76 000 GOs for green or low carbon hydrogen, out of which 3 600 were used by 2019.

This was a pilot project covering less than 0.05% of the total EU market and less than 4% of the certificates were actually from renewable energy. Table presents this and other examples of GO certification schemes. In particular, such schemes should be used to track CO2 emissions from the production to the use of hydrogen, in order to recognise when and where the use of hydrogen can be more effective for decarbonisation purposes than direct electrification or the use of bioenergy**.

*For the purpose of this report, GO is used to define all schemes quantifying the GHG emissions of hydrogen or its derivatives.

**This is applicable to all advanced renewable fuels, including hydrogen and its derived products

POLICY PILLAR 4: GOVERNANCE SYSTEM AND ENABLING POLICIES

As green hydrogen transitions from niche to mainstream, the policies that drive the transition must not only cover the deployment of green hydrogen, but also its integration into the broader energy system.

It is economy-wide policies that affect the sustainability and pace of the transition.

Civil society and industry must be involved in this new sector in order to reap its benefits.

A broad base of support can create an enabling environment for green hydrogen actors to provide their value to the whole energy and social system. With these goals in mind, concrete actions that policy makers can take include

- Seeking advice from civil society and industry.

- Implementing measures to maintain industrial competitiveness and create export opportunities

- Identifying economic growth and job creation opportunities

- Introducing hydrogen as a part of energy security

- Setting international codes and standards

- Building or repurposing infrastructure.

- Ensuring access to financing

- Collecting statistics

Supporting Policies

Green hydrogen is at an early stage in most applications and needs policy support to advance from niche to mainstream and be part of the energy transition.

Some barriers to the deployment of green hydrogen in various sectors are relatively consistent across end uses, the cost barrier being the main one.

Other barriers are more sector-specific and call for a tailored approach.

Once priorities are set, policy makers need to address the barriers specific to the sectors where green hydrogen is expected to be deployed.

POLICY SUPPORT FOR ELECTROLYSIS

- Setting targets for electrolyser capacity

- Tackling high capital cost.

- Improving tax schemes for electrolysers.

- Paying a premium for green hydrogen.

- Ensuring additionality of renewables generation.

- Increasing support for research

POLICY SUPPORT FOR HYDROGEN INFRASTRUCTURE

Realising the potential of green hydrogen will require careful policy attention to meet the challenges of transport and storage.

It is important to begin now to plan the infrastructure of the future; similar to the planning of the power grid, the effects of such planning will be seen decades from now.

Policy makers should consider:

- Kicking off international collaboration on global trading of hydrogen

- Identifying priorities for conversion programmes

- Aligning standards and blending targets

- Financing infrastructure development

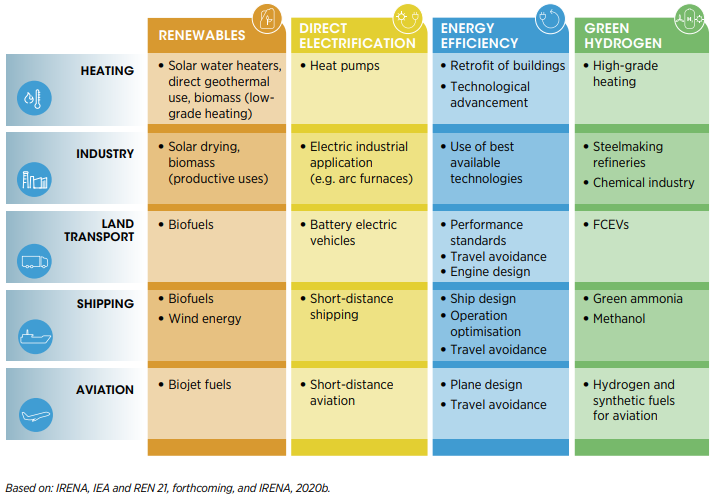

POLICY SUPPORT FOR INDUSTRIAL APPLICATIONS

Converting to green hydrogen can significantly reduce carbon emissions from the industrial sector, which is currently responsible for about one-quarter of all energy-related CO2emissions (or 8.4 GtCO2/yr). Four industries in particular – iron and steel, chemicals and petrochemicals, cement and lime, and aluminium – account for around threequarters of total industrial emissions (IRENA, 2020b).

Grey hydrogen is currently used as a feedstock to produce methanol and ammonia. Green hydrogen could replace much of it with no changes in equipment or technology, eliminating the emissions associated with the production of grey hydrogen.

Over 70% of global steel is produced via the blast furnace/basic oxygen furnace (BF-BOF) route, which relies mostly on coal. Most of the remaining steel is produced from direct reduction of iron (DRI) or steel scrap in an electric arc furnace (EAF), with fossil fuels providing both the reducing agent and energy for DRI and the electricity for the furnace. A structural shift in iron and steel making is needed, with renewables displacing fossil fuels for both energy and reducing agents.

One option is to apply alternative processes that can use renewable energy and green hydrogen (IRENA, 2020b)

POLICY SUPPORT FOR SYNTHETIC FUELS IN AVIATION

Aviation accounts for 2.5% of global energyrelated emissions. It is dependent on high energy density fuels due to the mass and volume limitations of aircraft.

Synthetic jet fuels produced from green hydrogen could play a role as drop-in fuels, complementing biojet fuels in decarbonising the aviation sector (IRENA, 2020b). Synthetic jet fuels are produced from hydrogen and a source of carbon (usually in the form of CO or CO2) and are hydrocarbons with the same physical properties of refined products from fossil fuels.

The amount of synthetic fuel needed for aviation (and thus the overall cost of the energy transition of the aviation sector) could be reduced further through greater aircraft energy efficiency, lower demand for longdistance travel (e.g. through shifts to trains or reduced air travel, wider use of teleworking and teleconferencing), and direct electrification of short-haul flights. Electric propulsion could be feasible for small planes and short-haul flights.

The direct use of hydrogen in airplanes is also under consideration.

To take advantage of the opportunity to cut emissions from aviation using synthetic fuels, policy makers can consider:

- Setting explicit targets for reducing emissions in aviation

- Focusing more on synthetic fuels

- Providing financial incentives to reduce the cost gap between fossil fuels and synthetic fuels.

- Guaranteeing a sustainable carbon source

POLICY SUPPORT FOR HYDROGEN IN MARITIME SHIPPINGS

Maritime shipping is already the most efficient form of freight transport; it uses 30% less energy for a given weight and distance than rail transport and 90% less than heavy-duty trucks. But the 95 000 ships currently in use, which carry 80-90% of all global trade, emit substantial amounts of CO2 – 930 MtCO2 in 2015, equivalent to 2.8% of total global energy-related emissions. With heavy fuel oil providing more than three-quarters of the fuel used by ships, ships are also major emitters of sulphur, particulates and other air pollutants (IRENA, 2020b).

Around 20% of the global shipping fleet is responsible for 85% of the net GHG emissions associated with the shipping sector. Therefore, a limited number of interventions might have a large impact in decarbonising the shipping sector. Electrification via batteries or fuel cells could play an important role for shortdistance vessels. Biofuels are an immediately available option to decarbonise the shipping sector, either in blends or as drop-in fuels.

However, their potential is currently limited (IRENA, 2020b).

Green hydrogen could play an important role, but its adoption would require substantial adaptations to existing onboard and onshore infrastructure. In addition, green ammonia is emerging as one of the most feasible lowcarbon fuel pathways. Leading manufacturers are working on engines that can run on ammonia and are anticipated in 2024.

Many of the policies already described to reduce the cost gap between fossil fuels and green hydrogen and its related fuels will also help make these green synthetic fuels more economically viable for use in ships, from carbon taxes to economies of scale that bring down the price of renewable electricity and ammonia plants.

Beyond those general policies, there are specific steps that governments can take to accelerate the decarbonisation of maritime shipping. While these policies can be implemented either domestically or internationally, they will have the greatest impact at the international level. Policy makers should consider:

- Implementing fiscal incentives.

- Creating demand for green maritime fuels.

- Support infrastructure development

- Support international policy and regulations

Sources : Adapted by IRENA

To see more : IRENA – Green Hydrogen a Guide to Policy Making