Given that renewable and low-carbon hydrogen will be essential to support the decarbonisation of the energy system, it is important to identify and assess the opportunities offered by large-scale deployment of hydrogen in view of possibly integrating them into future updates of the national climate and energy planning and roadmaps towards a low-carbon energy system.

This study aims to analyse the role of renewable and low-carbon hydrogen in the National Energy and Climate Plans (NECPs), and to identify and highlight the opportunities for hydrogen technologies to contribute to effective and efficient achievement of the 2030 climate and energy targets of the EU and its Member States. Next to the information from the NECPs, additional publicly available material and

the consultant’s proprietary analytical tools were used. The opportunities for and impacts of hydrogen deployment are assessed per Member State and are summarised in individual fiches per Member State.

This information should contribute to ensuring that attractive options for using hydrogen technologies are duly considered by the Member States.

This report provides an analysis of the NECPs for 2021-2030 submitted by the EU Member States. The analysis focuses on the extent to which hydrogen deployment is addressed by the NECPs, and provides an overview of the hydrogen related targets, policies and initiatives covered by the NECPs.

Further, the report includes an opportunity assessment regarding the deployment of hydrogen technologies. The opportunities identified are mainly based on the technical potentials and existing infrastructure per Member State and reflect the national potential for hydrogen deployment, based on the three pillars of the value chain: production, delivery (transport, distribution and storage), and use/demand. The fourth influencing factor addresses the political and industrial environment in a qualitative way as an enabler for hydrogen deployment.

Finally, the report presents an overview of the national impacts of deploying renewable hydrogen. This includes estimates of 2030 hydrogen demand in a low and a high scenario in the EU Member States (plus UK) in the sectors industry, built environment, transport and power, and the resulting impact in terms of greenhouse gas emission reductions, infrastructure implications as well as security of energy supply, financial impacts, employment and value added.

As a whole these assessments can support Member States in determining or adapting their hydrogen policies and targets for 2030 and beyond and how to enable hydrogen deployment with the right set of policy measures. National teams working on decarbonisation roadmaps and updates of the NECPs are welcome to consider the opportunities and benefits of hydrogen deployment identified in this study.

The scenario assessment shows substantial potential benefits of hydrogen deployment by 2030.

The main assumptions and results are hereafter briefly presented.

Hydrogen demand

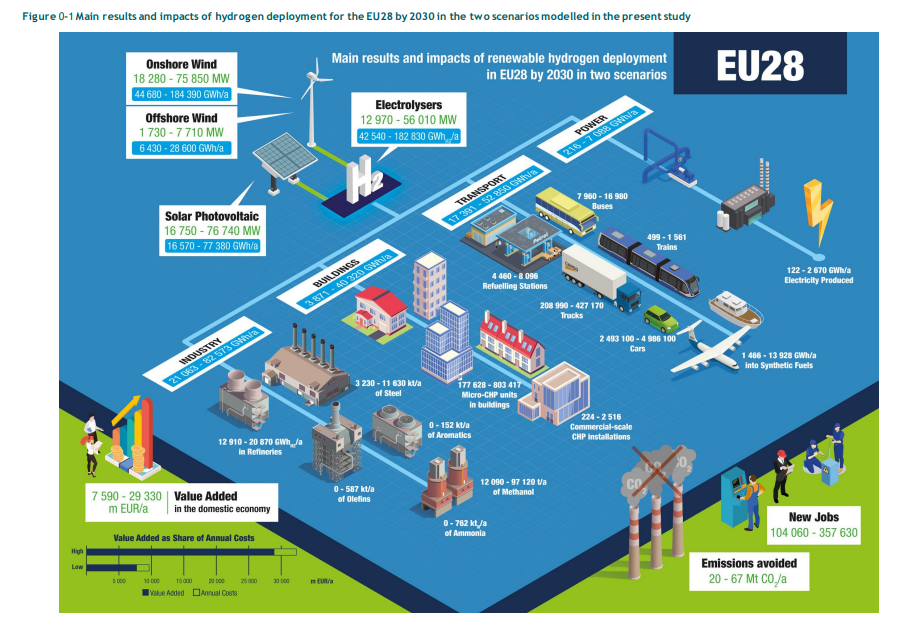

Two (high and low) scenarios of hydrogen demand in 2030 (42 and 183 TWh/a respectively for EU28) are developed, based on different levels of ambition linked to the national context in each Member State.

For most EU Member States, a significant increase of hydrogen demand is assumed in transport, especially for passenger cars, buses, trucks and trains, and to a limited extent in aviation (through hydrogen-based liquid fuels or Power to Liquid) and inland navigation. A significant increase of hydrogen demand is also assumed in industry (especially in refineries, chemical industry and the iron and steel sector). Some industries use at present fossil-based hydrogen as feedstock or as reducing agent, which could be replaced by renewable hydrogen. Switching high temperature heat processes fuels to renewable hydrogen represents another important potential use considered in the scenarios. In the building sector, hydrogen can replace part of the current use of natural gas ; it can in the short/medium term be distributed via existing gas grids through admixture to natural gas, and in the long term via dedicated networks. The building sector is expected to have in the low scenario a limited demand of hydrogen by 2030 but would have a stronger demand in the high scenario.

The scenarios assume only a marginal share of electricity generation from hydrogen by 2030, coming from combined heat and power installations.

Hydrogen production

To cover the hydrogen demand estimated in the 2 scenarios, 13 and 56 GW respectively of electrolyser capacity will have to be installed, assuming an average annual utilisation rate of 4.800 full load hours.

To this end, 68 and 291 TWh/a respectively of renewable power will be needed, based on an electrolysis efficiency of 69%. “Surplus” electricity from the markets in times of low electricity wholesale prices can be used for this purpose as well. However, the main share will have to be covered by dedicated renewable electricity sources. For three countries with a high readiness for CO2 storage, namely Germany, the Netherlands and the UK, low-carbon hydrogen produced via steam methane reforming (SMR) in combination with CCS is considered as an alternative. Although a combination of electrolysis and SMR production is expected to develop in practice, the study shows that SMR capacity of 2 and 9 GWH2 respectively, would be needed to fully replace the electrolysers and cover the corresponding hydrogen demand in these countries (16 and 74 TWhH2/a respectively).

Estimated socio-economic and environmental impacts

The annual costs to produce renewable hydrogen (including the cost of dedicated renewable electricity generation), to develop the transport infrastructure (or adapt the existing one) and end-user applications would in the considered scenarios reach 10 and 33 billion EUR, respectively. The cumulative investments needed up to 2030 would reach 70 and 249 billion EUR, respectively. These activities will generate value added in the domestic economy, amongst others , by creating jobs in manufacturing, construction and operation of hydrogen technologies estimated at 104 000 and 357 000 jobs respectively, and will contribute to greenhouse gas emission reductions. This is particularly important in hard-to-decarbonize energy uses, such as heavy-duty transport, steel production, refining or ammonia and methanol production. According to the European EUCO3232.5 scenario, there is a remaining gap of 1.5 GtCO2/a in emission reduction plans that needs to be closed in order to achieve 2030 goals. In the scenarios considered, the deployment of hydrogen could contribute 20 and 67 Mt

CO2/a respectively to this goal, which is equivalent to 1.4% and 4.6% respectively of the required emission reduction.

The following and infographic present the major outcomes from the scenario assessment.