On the demand side, too, hydrogen molecules are a critical complement to electrons in the challenge of far-reaching decarbonization. Our vision sees hydrogen powering more than 400 million cars, 15 to 20 million trucks, and around 5 million buses in 2050, which constitute on average 20 to 25% of their respective transportation segments. Since hydrogen plays a stronger role in heavier and long-range segments, these 20% of the total fleet could contribute more than one-third of the total CO2 abatement required for the road transportation sector in the two-degree scenario.

In our vision, hydrogen also powers a quarter of passenger ships and a fifth of locomotives on nonelectrified tracks, and hydrogen-based synthetic fuel powers a share of airplanes and freight ships.

For buildings, hydrogen builds on the existing gas infrastructure and meets roughly 10% of global demand for heat. In industry, hydrogen is used for medium- and high-heat processes, for which electrification is not an efficient option. Current uses of hydrogen as a feedstock are decarbonized through clean or green production pathways. In addition, hydrogen is used as renewable feedstock in 30% of methanol and about 10% of steel production.

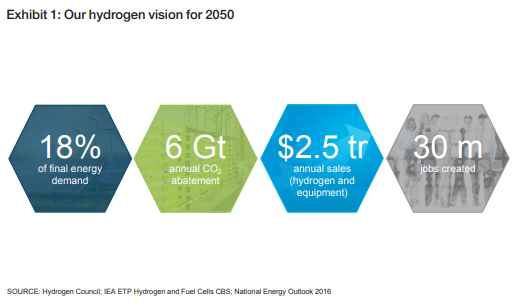

Achieving this vision would create significant benefits for the energy system, the environment, and the global economy. Across all seven roles, hydrogen could account for almost one fifth of total final energy consumed by 2050. This would reduce annual CO2 emissions by roughly 6 Gt compared to today’s technologies, and contribute roughly 20% of the additional abatement required to limit global warming to two degrees Celsius (above and beyond already agreed commitments). It would also eliminate local emissions such as sulphur oxides, nitrogen oxides, and particulates linked to smog formation, and reduce noise pollution in cities. The transportation sector would consume 20 million fewer barrels of oil per day, and domestic energy security would rise significantly

Alongside its environmental benefits, the hydrogen economy could create opportunities for sustainable economic growth. We envision a market for hydrogen and hydrogen technologies with revenues of more than $2.5 trillion per year, and jobs for more than 30 million people globally.

Getting there: A roadmap to the hydrogen economy

To realize this vision and achieve its desired impact, a significant step-up across the value chain would be required. Many of the required technologies are already available today – now is the time to deploy hydrogen infrastructure and scale up manufacturing capacities so as to achieve competitive costs and mass market acceptance.

In the transportation sector, hydrogen-powered FCEVs could complement BEVs to achieve a deep decarbonization of all transportation segments. FCEVs are best suited for applications with long-range requirements, heavier payloads, and a high need for flexibility. Decarbonizing these segments is particularly important as they consume a large share of total energy – while trucks and buses would account for only 5% of all FCEVs in 2050, they could achieve more than 30% of hydrogen’s total CO2 abatement potential in the transport sector.

Hydrogen can already lower the total cost of ownership of trains and forklifts, and we expect all transportation segments to be within a 10% range by 2030. These cost reductions require a significant scale-up of manufacturing capacities. If realized, FCEVs would have lower investment costs than BEVs in long range segments, with much shorter refueling times. Environmentally, FCEVs produce 20 to 30% less emissions than conventional cars even when hydrogen

is produced from natural gas without carbon capture; with renewable and clean hydrogen, FCEVs emit very little CO2 and require less resources and energy in the manufacturing process than BEVs.

FCEV buses, medium-sized cars, and forklifts are commercially available today. The next five years will see the introduction of more models in medium-sized and large cars, buses, trucks, vans, and trains, and it is likely that additional segments such as smaller cars and minibuses will follow until 2030. To realize our vision, 1 in 12 cars sold in California, Germany, Japan, and South Korea should be powered by hydrogen by 2030, when sales start ramping up in the rest of the world. More than 350,000 hydrogen trucks could be transporting goods, and 50,000 hydrogen buses, thousands of trains and passenger ships could be transporting people without carbon and local emissions. Towards 2050, our vision also includes hydrogen as a feedstock for renewable fuels for commercial aviation and freight shipping.

Large amounts of hydrogen are used as feedstock for refining and the production of methanol.

Decarbonization of these processes is starting, and with the right regulatory framework, the first oil refineries and ammonia plants could produce hydrogen from clean sources in 2030

In addition, hydrogen could be used together with captured carbon or carbon from biomass to replace fossil fuels as feedstock for the chemical industry.

By 2030, 10 to 15 million tons of chemicals could be produced from such renewable feedstock. In the iron and steel industry, where hydrogen can be used to reduce iron ore to iron, we expect the use of clean hydrogen will be demonstrated by 2030 and gain momentum by 2035.

For heat and power for buildings and industry, hydrogen can make use of existing gas infrastructure and assets. For buildings, low concentrations of green hydrogen could be blended into public natural gas networks without any infrastructure upgrades. Alternatively, entire cities could be converted to pure hydrogen heating. Both processes have already started and could start scaling up around 2030, with the equivalent of more than 5 million households connected to a gas network with blended or pure hydrogen. A second wave of commercialization could start once the costs of producing hydrogen have fallen enough to drive uptake in more cost-sensitive industry segments. While hydrogen penetration may not reach the same rates in industry as in other segments, industry’s large energy consumption implies substantial hydrogen demand beyond 2050. By 2030, up to 200 steel, chemical, and automotive plants could be pioneering the use of hydrogen for heat and power.

As the energy system relies more heavily on renewables, hydrogen could also play a growing role in the storage of renewable electricity and the production of clean electricity. Hydrogen allows to store and transport renewable electricity efficiently over long periods of time and is therefore a key enabler of the transition to renewable energy. By 2030, 250 to 300 TWh of surplus renewable electricity could be stored in the form of hydrogen for use in other segments. In addition, more than 200 TWh could be generated from hydrogen in large power plants to accompany the transition to a renewable electricity system.

What needs to be done: A call to action

To achieve this hydrogen vision, companies across the value chain will need to step up their efforts from hydrogen production and infrastructure to end-use applications.

Building the hydrogen economy would require annual investments of $20 to 25 billion for a total of about $280 billion until 2030. About 40% ($110 billion) of this investment would go into the production of hydrogen, about a third ($80 billion) into storage, transport, and distribution, and about a quarter ($70 billion) into product and series development and scaleup of manufacturing capacity. The remainder, some $20 billion, could go into new business models, such as fuel-cell-powered taxi fleets and car sharing, on-demand transportation of goods, and contracting of combined heat and power units. Within the right regulatory framework – including long-term, stable coordination and incentive policies – attracting these investments to scale the technology is feasible. The world already invests more than $1.7 trillion in energy each year, including $650 billion in oil and gas, $300 billion in renewable electricity, and more than $300 billion in the automotive industry.

Industry would have to bring down costs of hydrogen and applications through scale. Significant cost reductions have already been achieved in some areas; the cost of refueling stations and fuel cell stack production have been cut in half in the last ten years, for example. We expect major reductions in the coming years from scaling up manufacturing to industrial levels. Further cost reductions are also necessary to bring down the cost of hydrogen itself. These are possible through cost reductions in the hydrogen production and renewable power generation for electrolysis.

To start down the road to a hydrogen economy, we propose large-scale deployment initiatives supported by long-term policy frameworks in countries that are early adopters. These deployment initiatives should use current activities as platform and scale their successes nationally and, at a later stage, globally. In the transportation sector, we propose a three-phased deployment plan at national level, led by an overall roadmap and targeted support to ramp up the infrastructure and deploy more vehicles. In building heat and power, we propose to replicate the approach taken in the UK, which is investigating a city-by-city transition from natural gas to hydrogen. For industrial applications, we propose to support large-scale pilots in steel manufacturing, power generation, and clean or green hydrogen feedstock for the chemicals, petrochemicals, and refining industries. Once these technologies are proven, a long-term regulatory framework should be put in place to promote uptake. A critical factor here is a fair distribution of costs so that competitiveness and employment are not compromised in industries exposed to international trade.

The sector-specific deployment initiatives should be synchronized to achieve additional synergies. We propose to build national action plans, such as those in Japan, for the adoption of a hydrogen economy. These plans should have clear targets, specific deployment initiatives, and be underpinned by a long-term regulatory framework to unlock investment.

The 18 steering members of the Hydrogen Council, who represent companies with a combined market capitalization of more than $1.15 trillion, are working towards making this vision and roadmap a reality. Our research shows that hydrogen is an essential element in achieving deep decarbonization of the global energy system at scale.

We believe the world cannot afford to put off the efforts required to reach our common goals of deploying hydrogen and limiting global climate change as agreed in Paris in 2015. We hope to accelerate this transformation and are looking forward to investors, policymakers, and businesses joining us on this journey.