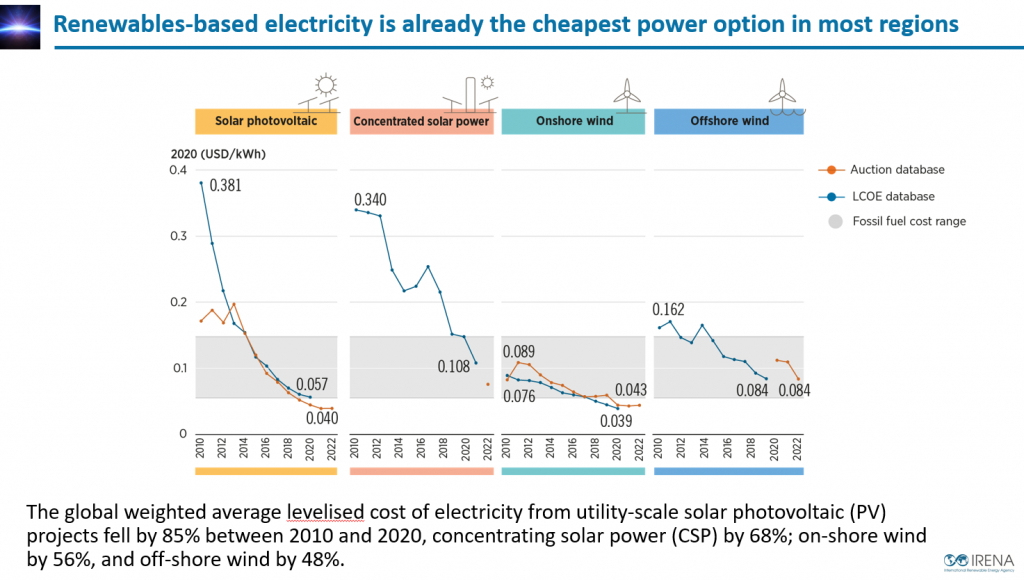

Climate change, energy security, energy access and air pollution have placed a renewables-based energy transition at the forefront of the national, regional and global discourse. Addressing those problems using renewables will be indispensable if policy makers are to limit the global temperature rise to 1.5°C by 2050, with net zero CO2 emissions. Fortunately, renewables are increasingly the lowest-cost source of electricity in many markets, capping a remarkable decade of change for renewables-based generation of electricity, during which the cost of utility-scale solar PV, for example, fell by 85%. The momentum of renewable energy is further demonstrated by its resilience in the face of the COVID-19 pandemic.

Falling costs have prompted a substantial rise in capacity, to the point where renewable power technologies now dominate the global market for new generation capacity. To meet the challenges posed by greater shares of solar and wind energy in the power mix, rapid advances have been made in digital technologies, battery storage, and new business models.

Policy instruments have evolved apace, with competitive pricing quickly overtaking administratively determined tariffs. The number of countries adopting renewable energy auction schemes increased from 16 in 2010 to 109 in 2020, driving down the average price of solar energy. The number of countries with renewable energy policies has grown as well.

In 2019, 143 countries had policies for renewables in the power sector compared with 117 in 2014.

Climate change, energy security, energy access and air pollution have placed the energy transition at the forefront of the national, regional and global discourse

In 2020, investment in the global energy transition hit a record high. Investments in electrified transport are also on the rise, as policies supporting the electrification of transport gain traction.

Policies for the use of renewables in heating and cooling have received less attention, though signs of progress are abundant.

Despite their growth overall, renewable energy investments remained concentrated in a few regions and countries. The Asia-Oceania region, led by China, regularly attracts the largest share of renewable energy investment (on average, 55% during 2005-2019). Europe and the United States follow, with average shares of 20% and 16%, respectively, during 2005-2019. Regions dominated by developing and emerging economies remained consistently under-represented, attracting only about 15% of global investments. Yet, annual financial commitments to off-grid renewables

supporting energy access in emerging and developing countries reached USD 460 million in 2019, up from only USD 6 million in 2008.

Overall, most renewable energy financing is provided by the private sector – 86% in 2013-2018.

Private capital came mainly from project developers (46%) and commercial financial institutions (22%). To date, conservative institutional investors have provided only a small share of financing, though this is expected to change as the perceived risks of investment in renewables fall.

Although public finance accounts for only 14% of total direct investments in renewable energy assets, considerable public resources are spent to create an enabling environment for the deployment of renewable energy through the promulgation of regulatory instruments, fiscal incentives, and other policies and measures. Public financing resources are crucial to lower risks, overcome initial barriers, attract private investors and bring new markets to maturity. As such, they play an especially vital role in emerging and developing countries where, aggravated by the COVID-19 crisis, investors’ risk perception is comparatively high.

The time dimension is crucial and a radical shift is required based on readily available renewable energy and energy efficiency technologies that can be scaled up now

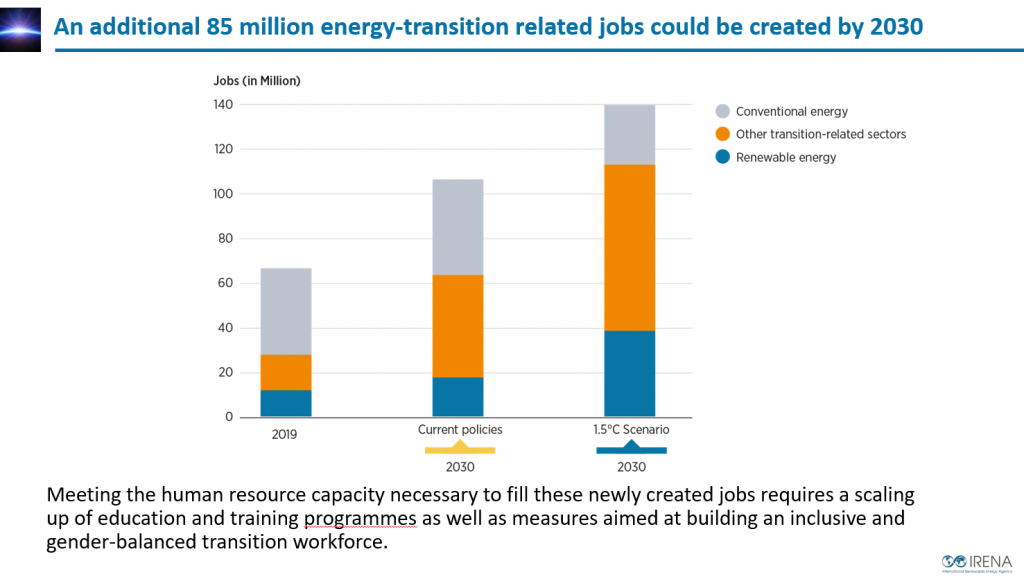

The progress achieved in deploying renewable energy has yielded impressive socio-economic benefits over the past several years, notably job gains all along the value chain. Most of the new jobs are found in the countries that are the leading markets for the installation and manufacture of renewables-related equipment. But employment is also being created in construction and in operations and maintenance across a wide range of countries.

The full impact of the COVID-19 pandemic on employment in renewable energy is not yet known, but renewable energy fared well compared with conventional energy. In many countries, a cycle of delays in spring 2020 was followed by great surges of activity later in the year. These impacts reinforce the importance of a comprehensive policy framework to align short-term recovery needs with long-term decarbonisation pathways and to ensure steady socio-economic benefits and a just transition.

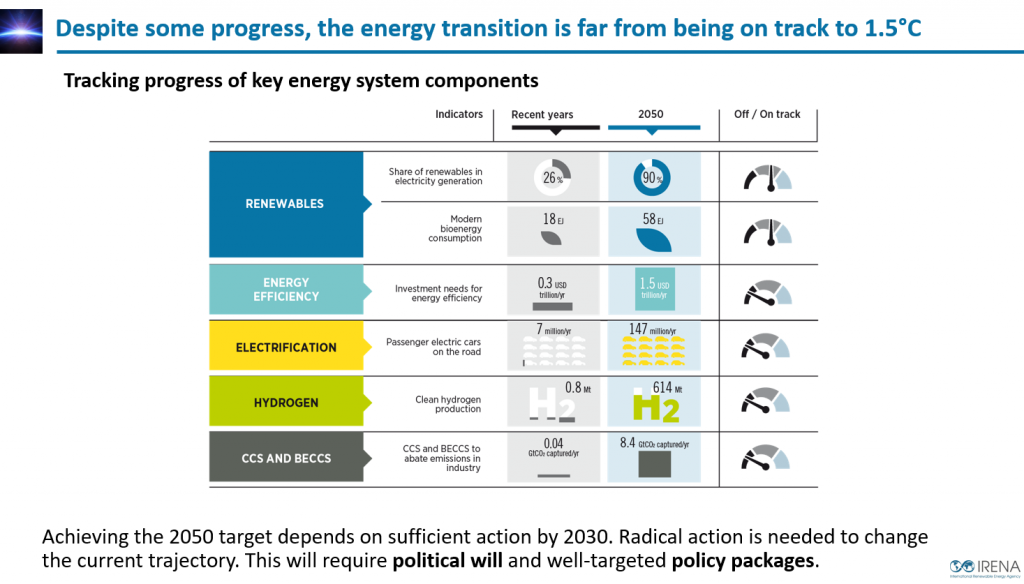

Trends to date have shown the way towards a decarbonised sector in 2050 but they have had little or no effect on rising emissions. Indeed, progress still falls woefully short of what is needed to hold the rise in global temperature to 1.5°C by 2050. The time dimension is crucial and a radical shift is required based on readily available renewable energy and energy efficiency technologies that can be scaled up now. IRENA’s 1.5°C Scenario starts with the goal of reducing global CO2 emissions by following a steep and accelerated downward trajectory from now to 2030 and a continuous downward trajectory thereafter, reaching net zero by 2050. This is achievable but extremely challenging, requiring urgent action on multiple fronts, as explored in detail in Chapter 2.

Sources : IRENA – World Energy Transition Outlook (1.5 °C Pathway)

Technological avenues to climate targets

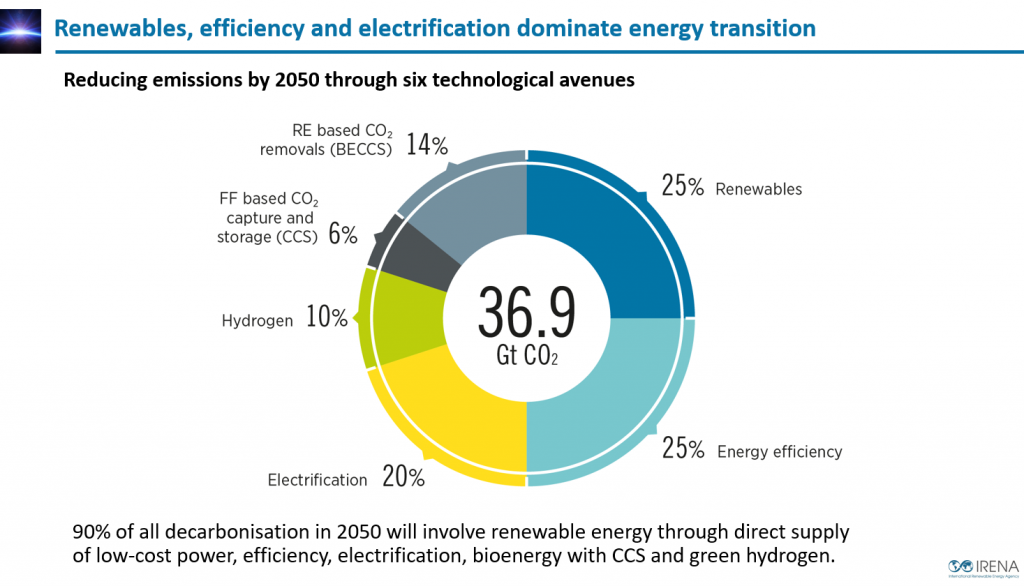

IRENA’s analysis shows that over 90% of the solutions shaping a successful outcome in 2050 involve renewable energy through direct supply, electrification, energy efficiency, green hydrogen and bioenergy combined with carbon capture and storage (BECCS). The technological avenues leading to a decarbonised energy system have crystalised, dominated by solutions that can be deployed rapidly and at scale. Technologies, markets, and business models are continuously evolving, but there is no need to wait for new solutions. Considerable advancement can be achieved with existing options. But taking the energy transition technologies to the necessary levels, and at a speed compatible with a 1.5°C goal, requires targeted policies and measures.

Too see more : World Energy Transition Outlook (1.5 °C Pathway)